Most of the time we receive market updates and published reports that are not audio-focused, or not detailed enough to be newsworthy - and one would have to actually purchase the full document in order to extract the information relevant to an audio industry audience. Even with most press releases, we need to expand beyond the general headlines - which is what market research firms (understandably) use to sell their services, but not enough for publication.

audioXpress is focused on serving the audio industry, and we are more interested in providing market intelligence than publishing subjective opinions about the measurement systems used by YouTube headphone reviewers - which seems to be the latest focus even for many competent audio publications these days. As I wrote last week, we normally reserve essential market analysis for our magazine Market Update features. But sometimes, by cross referencing market research headlines and overviews, we can identify interesting trends, useful at critical moments such as now, with the post-pandemic economy.

I'll start by noting the latest report we received from market advisory firm ABI Research, announcing that the Consumer Device Market is Set for Meteoric Post-Pandemic Growth. The firm's latest report covers a wide range of consumer product segments, focusing as usual on smartphones and 5G in particular. The part that caught our attention was the specific reference to voice control front-end devices, which, like wearables, are said to be ready for "explosive growth" in 2021.

ABI Research highlights the standard context of the COVID-19 pandemic, and the disruption to production lines and supply chains, adding the market for consumer technologies remained resilient in 2020, and that some specific segments, like video streaming devices, or home networking, even saw shipments accelerate - "as the impact of the pandemic starts to wane, consumer confidence returns, and device supply chains bounce back to near- pre-COVID levels."

Interestingly, this ABI Research report highlights consumer devices supporting Ultra-wideband (UWB) connectivity - which is an area that we have been following closely and that I would strongly recommend all audio manufacturers do the same. UWB has a lot of potential use cases for our lifestyles, which will also have an impact on audio products, helping among other things to improve user identification, personalization, and fast pairing/parametrization of devices.

Also, UWB has the potential to augment the "smart" in smart speakers. "...ultralow-power machine learning (ML) chipsets and devices supporting ultra-wideband (UWB) are among the major consumer technologies that will take-off this year,” expands Khin Sandi Lynn, Industry Analyst at ABI Research.

Moving on

ABI Research estimates that the wearables and true wireless headsets market will see explosive growth, overcoming 1 billion shipments in 2025. That's 1,000 million devices: "...the wearables and true wireless headsets market will see explosive growth in the next 5 years, overcoming 1 billion shipments in 2025. These devices are evolving from simple smartphone accessories to whole digital platforms, providing personalized and high-quality experiences that empower user’s daily activities," says Lynn.

This ABI research report also confirms another important trend that we have already been highlighting in audioXpress for years. The need to think about connected systems in a broader view. "Ultimately, the consumer technology market is starting to shift from being device-centric to one that is experience-focused. Cloud services and the range of Internet-connected content and apps, increase the value of available personal consumer devices and smart home appliances and drive purchase decisions.

"Consequently, consumer electronics and device vendors need to build ecosystems that offer consumers flexibility and seamless experiences, combining hardware quality, platform-agnostic content, and cloud services," states Eleftheria Kouri, a Research Analyst at ABI Research.

IDC is optimistic about the strong potential for fitness wearables with advanced health sensors and hearables in particular. "2020 was the year that hearables became the must-have device," says Ramon T. Llamas, research director for IDC's Wearables Team. "Hearables provided a new degree of privacy, particularly during home quarantine but also while out in public. Meeting that demand was a long list of vendors with an equally long list of devices, spanning the range of feature sets and price points. Underpinning the hearables market was a constantly shifting competitive landscape, with companies slowly gaining a foothold in the market (Amazon and its Echo Buds and Frames), vendors introducing new form factors (Apple and AirPods Max), and new features making their way down the price curve, including automatic noise cancelling and voice assistant capability."

Without having access to actual sales figures in these categories from the brands, and with estimates diverging widely, all market research firms still conclude that Apple's lead and market share remains massive both for the two AirPods models, and certainly for the Apple Watch. The remaining market is mostly disputed by Chinese brands, selling very low price items, and making hardly any margin, while cutting into the more serious efforts by Amazon, Google, Samsung, Huawei and all the others major manufacturers in that space.

While everyone agrees that hearables and wearables will soon mostly rely on edge AI and will cut the wireless cord from smartphones, the reality today is that the category mostly depends upon smartphones to remain connected, and serves as an extension to the "computer in the pocket" or "on the wrist". For now, it remains a question of how much battery a device can hold - and it's more than certain that big and heavy earbuds on our ears is not an appealing concept for consumers. In fact, artificial intelligence on-device (that doesn't rely on connected cloud services such as personal voice assistants mostly do today) is a concept that is now being perfected directly on the smartphone itself. In a few years, it will be able to transition to wearables in general, and hearables.

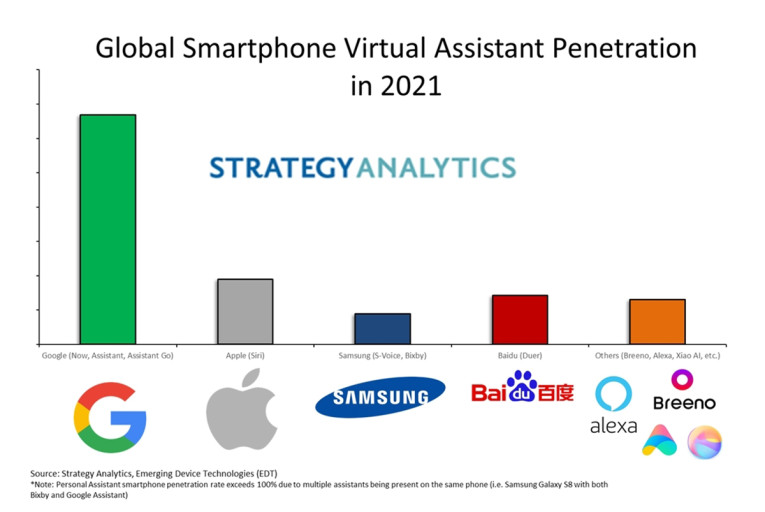

In its latest "Smartphones: Global Artificial Intelligence Technologies Forecast to 2025" report, Strategy Analytics signals that on-device AI is being rapidly implemented by smartphone vendors for important things such as power optimization, imaging, enhancing device performance, and of course, to optimize personalization and interactions with voice assistants. "The push to add on-device AI computational power to enable Edge AI computing is a priority for smartphone and chipset vendors," notes the market research firm.

So, before we will truly have intelligent earbuds, the industry will perfect edge AI on the more powerful and less power restricted platforms currently available, which are smartphones. “Strategy Analytics estimates that 71% of all smartphones sold worldwide in 2021 will have on-device AI,” says Associate Director Ville-Petteri Ukonaho. “Advantages of on-device AI computing include lower latency, better data privacy, and overall lower power consumption.”

In the future, edge AI features will be able to completely support personal voice assistants, and this is now being perfected on smartphones. "Modern smartphones give consumers access to their own personal AI powered super-computer," says Ville-Petteri Ukonaho. "With the help of on-device Artificial Intelligence, virtual assistants like Siri and Google’s Assistant have become more intelligent and aware of their environment."

What this report doesn't mention (at least in the brief information available) is the fact that true wireless earbuds are in practice already used as vital extensions for those smartphone-powered AI features. Sensors placed directly in the ear can convey a level of data that is essential to personalization and augmentation features, while voice front-ends placed in hearables are the seamless interface that overcomes most of the barriers for human interaction.

Also according to Strategy Analytics, the global smartphone applications processor (AP) market returned to revenue growth in 2020. The company estimates that Qualcomm (31%), Apple (23%), HiSilicon (18%), MediaTek, and Samsung LSI grabbed the top-five revenue share rankings, while TSMC led the smartphone AP foundry market with more than two-thirds of the market share in 2020, followed by Samsung Foundry. Both foundries saw strong demand for 7nm and 5nm APs. Compared to the volumes these processors achieve in smartphones, applications such as wearables are still not very significant, but that will change over the next five years.

And one of the reasons for the transition to edge AI, and the expansion of processing power in hearables, is directly related to the previously mentioned quality of the connected experience. As Strategy Analytics also reports, devices are becoming increasingly smart, connected, and automated to form progressively more complex ecosystems to offer product and service combinations to consumers. This increased complexity and interconnectivity between devices presents many new challenges for user interfaces and the overall user experience (UX). "A product can no longer be designed in isolation. Connected systems such as smart homes, autonomous vehicles, and wearables need to be designed for a larger connected universe of services, devices, and sensors, and in many cases, incorporating different ecosystems," notes Lisa Cooper report author and Director, User Experience Strategies at Strategy Analytics.

Speakers are doing nicely, thank you. But doing even better are smart speakers. According again to Strategy Analytics, global smart speaker sales reached a record level in 2020 - 150 million units - in spite of the challenging conditions. New model introductions from Apple, Amazon, Google, Alibaba, and Baidu, all hitting the market in time for the holiday shopping season, contributed to a positive end to a difficult year. Smart displays accounted for 26% of the total smart speaker market during the quarter, up from 22% in Q4 2019.

Amazon led the overall smart speaker market in Q4 with a 28.3% share of global shipments; Google finished second with a 22.6% share of the market; Baidu and Alibaba finished the year strongly, with solid double-digit shipment growth; and Apple was the standout performer in the quarter as its global shipments grew by 74% year-over-year following the launch of the $99 HomePod Mini in November 2020.

Looking at another related report by Parks Associates, 34% of the US senior broadband households (heads of broadband household ages 65 and older) already have a smart speaker or smart display, as the low product cost and convenience of voice-first interfaces continue to spur rapid adoption. Current adoption of smart speakers/smart displays is 49% among all US broadband households. So, definitely not a category where music listening is the top priority, or even a priority. In fact, smart speakers frequently replace "listening" to music on the tablet or smartphone speakers, offering a step-up experience (imagine that).

In a related report, Parks Associates announced that 25% of US broadband households bought at least one smart home device in the past 12 months and households with at least one smart home device now own on average more than seven devices. Product categories include smart thermostats, smart appliances, network cameras, video doorbells, smart smoke/CO detectors, smart door locks, smart garage door openers, and smart lighting products, among others. In all those houses, smartphones are still being used as the primary control interface, followed by smart speakers. So, lots of potential for growth.

As I previously wrote, unlike the original (and now discontinued) Apple HomePod, which was primarily focused on the music listening experience (an iPhone accessory essentially), the HomePod mini was touted by Apple as an actual Smart Speaker. In fact, betting on music listening, an intelligent assistant, smart home capabilities, and with built-in privacy and security - all for $99. Now, if someone offered a speaker with all that AND an 8" woofer (at least) plus another one for stereo pairing... I would actually want to buy one (two actually). So... maybe the HomePod could eventually return in an improved iteration.