This is extremely relevant considering that TSMC is the top producer of the world's most advanced processors, including the chips found in the latest Apple devices, and TSMC clearly says that "demand for consumer electronics has plunged post-pandemic."

The "chips" that this company manufactures are mainly used in smartphones, tablets, and laptops, and TSMC confirms that "Global demand for laptops and smartphones spiked during COVID-19 lockdowns, spurring smartphone and PC makers to stockpile chips. Now those companies are grappling with excess inventories as consumers cut back on purchases of these goods due to rising inflation. This has led to a fall in prices for chips."

Note: Supply and demand rollercoaster. Excess inventories

For more insight, let's look at a specific data source for computers, International Data Corp. (IDC). Its Quarter Global PC Shipments analysis says that the "overall weak demand has caused inventory levels to remain above normal for longer than expected. This includes finished systems at the channel level, as well as the supply chain."

IDC confirms that "no PC maker has been immune to the challenges presented by the market," except for Apple and HP, "all the leading companies experienced double-digit declines during the quarter. But Apple benefited from a favorable year-over-year comparison as the company suffered supply issues during Q2 2022 due to COVID-related shutdowns within the supply chain. Meanwhile, HP has faced an oversupply of inventory in the past year and is finally approaching normalized levels of inventory, allowing its growth rate to shine during this downturn.

Note: Inventory levels above normal.

And let's check the panorama of smartphones from another specialized source in that segment, Counterpoint Research. In its latest report for Q2 2023, this market intelligence company says that global smartphone sales are declining for the eighth straight quarter. "Global smartphones sell-through declined 8% YoY and 5% QoQ in Q2 2023." Samsung led the quarter, and Apple came in second with its share growing to 17% despite unfavorable seasonal factors. "Premium segment demand remained resilient, with the segment’s share reaching a Q2 record," Counterpoint states.

Interestingly, Apple is "reaching record shares in multiple new markets, which are typically not considered its core markets. A prime example is India, where it grew 50% YoY in Q2 2023. The continued strong performance of the premium segment has made sure that revenues don’t suffer as much as sales volumes, which is why brands are investing in market expansion and innovation in newer technologies."

Note: Premium segment demand remained resilient.

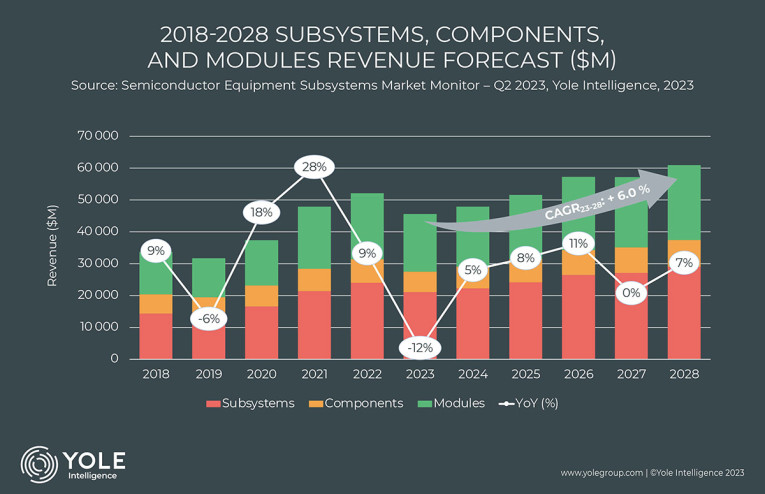

Finally, let's look at the overall semiconductor category. In this case, the resource will be Yole Intelligence, part of Yole Group, which reports in its Semiconductor Equipment Subsystems Market Monitor, that "While Q1 2023 experienced a significant market correction, signs of recovery are emerging just around the corner.

According to Yole, "the total market size reached $46 billion USD in 2022, with subsystems dominating the market share at 50%, followed by modules at 34%, and components at 16%." And apparently the panorama in this category is getting brighter. "Despite facing challenges in late 2022 and Q1 2023, suppliers have achieved remarkable growth over the past four years."

And these reports confirm that "the first quarter of 2023 posed significant challenges" because of "high inventory levels at OEMs," which led to "a sharp decline in order intakes during Q1." The expectation is that orders will gradually increase for the rest of the year driven by "anticipation for 2024, which holds the potential for the beginning of a new multi-year growth cycle..."

Note: Recovery around the corner.

By now, you will have noticed that any attempt to characterize the state of the economy for the audio industry is limited to reading the signs from what are apparently very distinct, broader product segments. Yet, understanding these larger and wide-reaching product classes enables a better understanding of the overall macroeconomic picture and trends in consumer behavior.

Considering that there aren't any market research firms doing field work in product categories that might be relevant for the audio industry (there used to be some, but it's been now more than 3 years since we've seen any relevant, credible market reports), this is the best we can use to understand the environment we are in. It's hard to understand that we haven't had any actionable market reports produced in major trending categories such as true wireless earbuds or hearables in the consumer space, or even in automotive audio. It's about time a serious market research company puts in the effort.

But overall, the biggest challenge to understand how the audio industry is doing continues to be its segmentation. Consumer products are completely divided in large segments such as personal audio (earbuds, headphones, portable music players, portable speakers, etc.) and in the broader segment of "home audio," one can find everything from system integration solutions to the cheap home-theater-in-a-box, soundbars, and Ikea wireless speakers. And within that same segment, we can look at the crazy business of high-end audio and hi-fi - which is a microcosm - or high-end home theater with private investments multiple times higher than what a commercial cinema auditorium typically costs to put in place.

There really isn't a single "audio industry," and audio products these days reach so many different markets and applications that the largest part of the business are components used in smartphones, laptops, TVs, cars, and by many other industries. But more important, one or way of another these different audio industry segments are all sourcing vital components and parts from the same stockpile, although they aren't necessarily conscious of each other, how much they compete, and how much they might depend upon the same suppliers.

That is why we really need a trade association that conducts serious research on the actual product segments that we know make sense, such as speaker drivers, audio amplifier components and modules, wireless audio modules, and more. This would help us to better understand what this industry is about and what business it actually moves.

From the opposite perspective, vital suppliers, such as semiconductor and electronic component manufacturers need to be closer to the audio industry and promote their own product portfolios. It's not acceptable that components that were designed and launched 20 or even 30 years ago (officially and unofficially EOL) continue to be specified and implemented in finished audio products, when much superior options from the same companies exist. We know that audio applications remain a relatively small niche for the large electronic companies, and there are never enough promotional and educational resources, but it’s not acceptable that new modern solutions remain relatively undisclosed to developers and audio companies (and even to specialized media such as audioXpress).

How Well Are We Doing?

I have been asked repeatedly in the past weeks, about "how the audio industry is doing" and "are we heading toward a contraction?" The anxiety comes from our already well-understood reliance on "outsourced manufacturing" which, like it or not, means China and will continue to mean China for the predictable future.

And what does China tell us?

According to the English-language newspaper South China Morning Post, we learn that the performance in China’s manufacturing sector is very concerning, as illustrated by the two latest purchasing managers’ indices (PMIs) - great indicators of economic health and gauging sentiment in the business sector. In these indices, any reading above 50 means growth in the sector.

The official PMI released by China's National Bureau of Statistics largely measures the sentiment among larger firms, many of which are state-owned. China’s official manufacturing PMI dropped to 35.7 in February 2023 from 50.0 in January, below the 38.8 figure reported in November 2008 at the start of the global financial crisis and indicating a sharp contraction in sector activity.

Last month, China’s official manufacturing purchasing managers’ index (PMI) rose to 49, from 48.8 in May. And the official non-manufacturing gauge, which measures business sentiment in the services and construction sectors, fell to 53.2 in June from 54.5 in May.

Clearly things are not going back to what they were pre-pandemic, and the manufacturing sector is at the heart of the contraction.

We tend to think that Western businesses are already moving to relocate production out of China, a process that began even before the US tariffs or the global pandemic. But the reality is that the Chinese manufacturers have been the first to initiate that same relocation, particularly for Vietnam and India, where we can already find factories from the larger OEMs and ODMs that the audio industry relies upon. The reopening post-pandemic in China has accelerated those moves, and one of the reasons is the lack of workers.

As the South China Morning Post illustrates, due to the impact of the pandemic, since 2020, manufacturers are struggling to resume operations. Many of China’s laid-off migrant workers in labor-intensive industries have shifted to other sectors and are not returning to their previous jobs. With the reopening, consumer spending increased and the country’s return to domestic travel and passenger traffic has exceeded pre-pandemic levels (although international travel has yet to recover). Now, economic activity in general is softening as recovery falters. After growing at a faster-than-expected pace in the first quarter, China's economy lost steam in April-June amid steepening deflation, disappointing retail sales, high youth unemployment, lower industrial production and... "sluggish foreign demand."

Note: Sluggish foreign demand

China is not receiving new orders as expected, and exports have slowed. Even the service sector recovery is losing steam from the post-pandemic levels. China's GDP is down, and uncertainty is the most common term used to describe what's going on in the country - much like everywhere else in the world.

Good News Is Bad News

We live in very unusual times, when we are facing completely new and unpredictable circumstances from the effects of a global pandemic that strangled the world for two whole years, and then when recovery was in sight, suddenly we were told to be afraid. Because of the unexpected and sudden inflation, central banks are responding with an "induced recession," which is frightening everyone - even if it might not happen.

When consumers were ready to party, they received a message that they should refrain from spending. When we all were getting ready to go back to travel, the raising inflation headwinds and predictions of recession stopped or reduced spending on many fronts. Yet unemployment remains at an all-time low and consumer spending remains strong. And consumers’ interests in new innovative products and technologies is at an all-time high, precisely because the pandemic has shown us all how useful and even essential those can be in our present lives.

As a result of the "induced recession" fears, orders are being put on hold and factories in China are not in any way busy. And when eventually orders resume, there are still many production lines that will remain constrained by labor and/or lack of components and parts.

In our specific sectors of the audio industry - admittedly small and niche - those concerns are not visible and demand for audio products has not diminished, much less "plunged" like in other product categories.

It might be useful to understand that it is impossible to project reliable trends in the audio industry without looking at the specific product segments. Understanding the manufacturers’ profiles and distribution channel strategies, how vertically integrated manufacturers are, and how resilient they are from these ongoing market disruptions and supply chain fluctuations. With the go-to-market strategies, how dependent from specialized retailers or dealers are they, or how much they rely on major online retailers - from Amazon to Sweetwater to Thomann - and how close are the products geographically and globally (e.g., as residential integration products tend to be)?

I see a world of difference between some companies in Europe who have most of their production in house, remain relatively conservative on technology updates, or simply rely on crafted materials (hi-fi speakers being a typical example) and for that fact they remain isolated from external supplier challenges and relatively immune from macroeconomic headwinds. Small audio electronic assemblers of professional audio or specialty hi-fi products suffered from some component shortages but have worked around it already since they have relatively small production volumes.

In some of those segments that I follow - and they can be as diverse as professional audio companies doing recording gear, or home audio companies doing integrated audio DACs/streamers - in most cases they are reporting a consistent and growing flow of orders, which they are being able to fulfill. The main reported challenges have to do with the need to redesign older products to meet consistent demand with existing parts, or delayed projects for new products precisely because of the need to manage resources.

Meanwhile, consumer electronics companies and others who predominantly manufacture in Asia have been holding on new large orders, afraid of the macroeconomic headwinds and the predicted recession - not realizing that they didn't yet sort their supply chain issues. And that when they will need to place volume orders again (likely wishing for a short delivery window), the factories in China they used to rely upon have moved on, some are struggling to keep production lines consistent for lack of workers or parts, and some might even have closed.

Some of the agile global companies I know, independently of the product space they target, have started sending their product managers and engineers to the field as soon as China reopened, or as soon as the pandemic effects receded, and traveling was advisable again. Those companies have prepared for both high demand/large volume production, as well as partitioned production schedules, closely managed with sales groups and the distribution channels. But more important, they all looked at the products they offered during peak demand pre-pandemic, or pandemic-generated, and quickly planned to renew their strategy to be able to offer innovations and new desirable designs - not more of the same.

Overall, we can say that the audio industry is relatively well positioned and resilient. The few examples of companies suffering and heading downward are typically the result of the success of others that are doing better. And there are obviously examples of companies making bad choices, as always.

The audio industry is benefiting from a series of innovations that are dependent on the implementation and adoption of new standards/specifications and technologies. The state of things I just described will delay those underlying innovations by delaying production roadmaps. We need to use the extra time to make sure that consumers are aware of the benefits when those innovations actually make it to market.

This article was originally published in The Audio Voice newsletter, (#430), July 20, 2023.