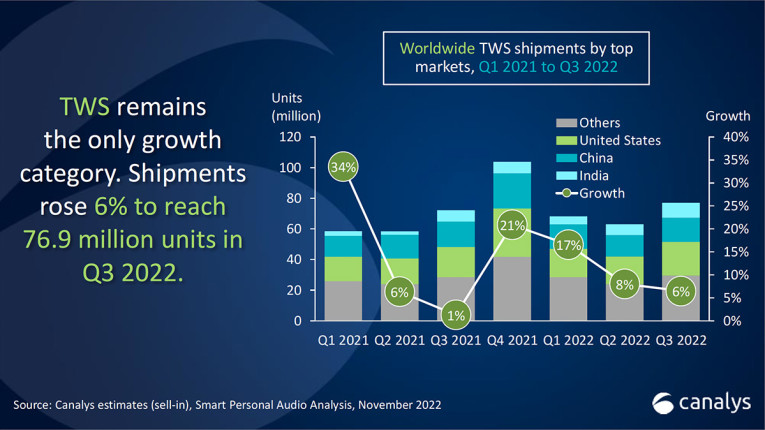

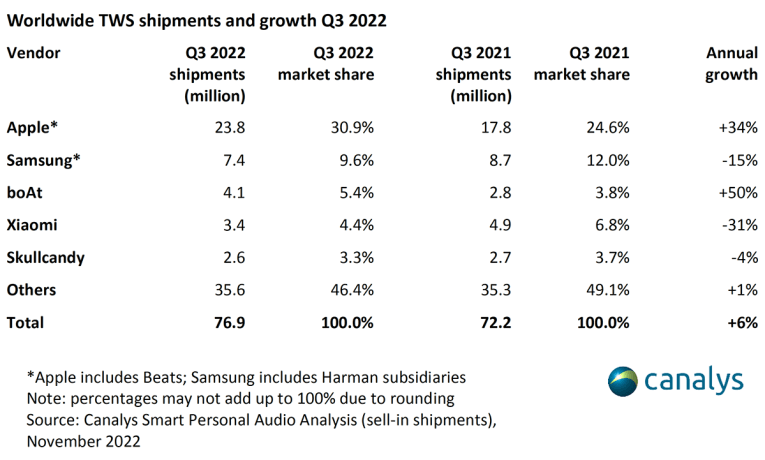

According to the latest Canalys estimates, the global smart personal audio market suffered its second consecutive decline in Q3 2022, with shipments down 4% to 113.6 million units. TWS remained the only category to show an increase, with 6% growth to 76.9 million units in the quarter. Apple (including Beats) defended its leadership position with the second-generation AirPods Pro launch, which led to a 34% increase in shipments and a 31% market share, according to the Canalys report. Samsung (calculated including its Harman subsidiaries, which is highly unlikely) took second place, “but its shipments fell 15% despite its new Galaxy Buds2 Pro launch,” its also stated. “India’s local vendor boAt took third place with a 5% market share, but its growth rate slowed to 50%,” is another strange fact added to the report. Skullcandy is identified as being fifth with 3% share, after a clone-brand from China - again not very likely given the geographical market coverage of the brands.

As it happens frequently with the market research data that is published by global firms - particularly over the past three years - these reports show confusing results that should be read with lots of caution. It seems that these firms are mostly outsourcing data collection to cheaper labour in India, where analysts have a very restricted and skewed perspective of the global market. And one of the most obvious signs starts with the unclear definition of what is considered in market categories, and a blurry line between units sold reported by some, units shipped from factory reported by others, revenue (which requires currency adjustments and are calculated with different criteria), and respective market shares.

First, Canalys defines the "TWS" market as “including wireless earphones and wireless headphones” - which is clearly confusing. If it does include “wireless headphones”, then the numbers don't make sense since there are distinct price segments and product segmentation for each. Second, the Canalys report includes India's brand boAT Lifestyle in the global results. Nothing against this very dynamic company, but its products are completely absent in most major markets even if it’s true that India represents large volumes - but so does the internal market in China. Also strange, the clone-brands from China that are mentioned in the report are clearly those that are active in India and a few other countries, but again clearly not that predominant in volume sales, given the intense market fragmentation in those cheaper price ranges, where there's hardly any brand recognition, never mind brand loyalty. We wouldn't be surprised to see Harman's JBL TWS products alone (not confused with Samsung’s own products) replacing the X brand that is mentioned in the actual market figures in the report.

Canalys does recognize the impact that the AirPods Pro second-generation launch had for Apple's market share, detailing that Apple shipped “4.2 million units” of that specific model, accounting for 20% of all AirPods shipments. Again, numbers to be taken with caution. Canalys reports says that Samsung, despite also launching its latest flagship model, faced a different situation as Galaxy Buds shipments fell by 25%. "The late August shipping date and the higher selling price of the Galaxy Buds2 Pro limited the market performance of the Galaxy Bud series in Q3," says Canalys research analyst Sherry Jin. “Samsung also took a more conservative approach in its bundling activities in Q3 to uphold the flagship positioning of its Pro series in its launch quarter,” Jin adds.

If accurate proportionally, and independently of the accuracy of the numbers quoted, what this report reveals is that there is very little brand loyalty in the category, apart from Apple and a few minor volume brands, and that not even Samsung, which ships a well-engineered product with a distinct design, is able to compete in the premium segment.

The Canalys report does illustrate well the situation in India, for those who need to follow that very unique market. "TWS shipments in India reached a new height of almost 10 million units in Q3 2022, while wireless earphone shipments recorded their first decline, of 20%. The TWS category share passed 50% for the first time, while the whole market’s growth rate slowed to 2%," the Canalys summary states.

"Local kings pushing these value-for-money devices and active market education (sic) will quickly accelerate the market’s transition to TWS," says Canalys analyst Ashweej Aithal. "But the single-digit growth rate of the whole market could reflect current market demand and consumption reaching a peak. When TWS shipments near the 10 million mark, local consumers will seek devices with better quality sooner or later, such as improved audio, longer battery life and ANC functions. Vendors must then be sensitive to this change in the market to provide improved devices and adjust their future shipments to maintain healthy inventory levels."

Adding a bit more perspective about the data in the report, Canalys says that in Q3 2022, audio-centric brands, such as Sony, Jabra and JBL (under Samsung’s Harman subsidiaries), used aggressive discounting across channels to sustain shipment levels, significantly weakening the market performance of value-for-money brands. "But these brands’ market value increases are relatively flat, which reflects the macroeconomic pressures that vendors are under. In Q4, market performance could continue to decline. As compared with last year’s shipment levels, most vendors will be more cautious, hoping to avoid excessive inventory levels. Aggressive discounting will only ease the pain in the short term. Vendors must dive deep and expand their user bases while maintaining their current advantages to hold share and survive into the future."

The report mentioned is part of Canalys’ Smart Personal Audio Analysis service.

audioXpress own reading of the data revealed in the text summary shows that it continues to be extremely difficult for audio brands to truly gain global market scale. It also indicates that brands should not define their strategies for the occasional success gained in some very specific regional markets, such as India or even Spain. When it comes to marketing a brand, the "Think Global, Act Local" concept remains the best approach, at par with the obvious "don't sell clone-product clones at the cheapest price possible" - it only makes consumers more aware of the value of the more expensive good-quality products. It might be true that many cannot afford to buy products in the premium price range, such as those from Apple, but their desirability is precisely what makes them valuable.

www.canalys.com