With an unprecedented growth period, MEMS sensors and actuators, which obviously include MEMS microphones and MEMS speakers, among many other application-oriented devices, have become part of everyday life and are found in a variety of systems. In 2021, revenues were driven by the continuous "sensorization" of both consumer and automotive applications and advances in the medical and industrial end markets and associated applications.

Secondly, ASPs of some MEMS devices, such as inertial and pressure MEMS, increased slightly in 2021 due to the chip shortage and global allocation problems, creating additional revenue growth in the market.

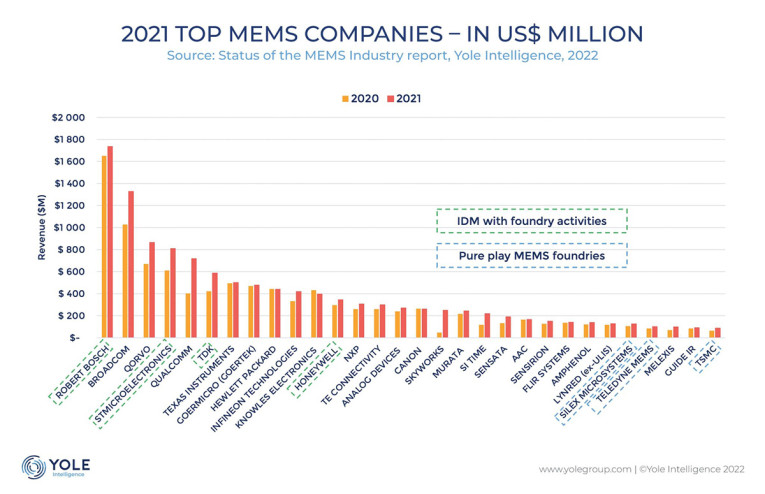

But who is supporting and profiting from the current and future growth? "Of course, mainly the incumbents in the top-10, which has not changed drastically in the past couple of years: Bosch, Broadcom, STMicroelectronics, Qorvo, TDK, Goermicro, Texas Instruments, HP, Infineon, Knowles, etc.," Damianos adds. "But let us not forget the long tail of other smaller specialized MEMS players, also poised to enjoy growth owing to emerging MEMS devices and applications: SiTime, USound, xMEMS, OQmented, Sensirion, etc," he reinforces.

Ensuing the unprecedented demand for MEMS sensors, MEMS players are currently investing in new production fabs: Bosch, SilTerra, Silan Microelectronics (160kwpy), and FormFactor. However, increasing capacity is currently the general trend in the semiconductor domain following the chip shortage, and the equipment market is fully saturated with high equipment prices and >15 months’ delivery times.

Acquiring MEMS businesses from other companies may be an option. Yole Intelligence’s analysts identified several significant examples: Silex acquired Elmos' 200mm wafer line, and Mitsumi acquired Omron’s MEMS business. In parallel, Bosch announced the construction of a 300mm MEMS line that will open in 2026 to consolidate its leading position.

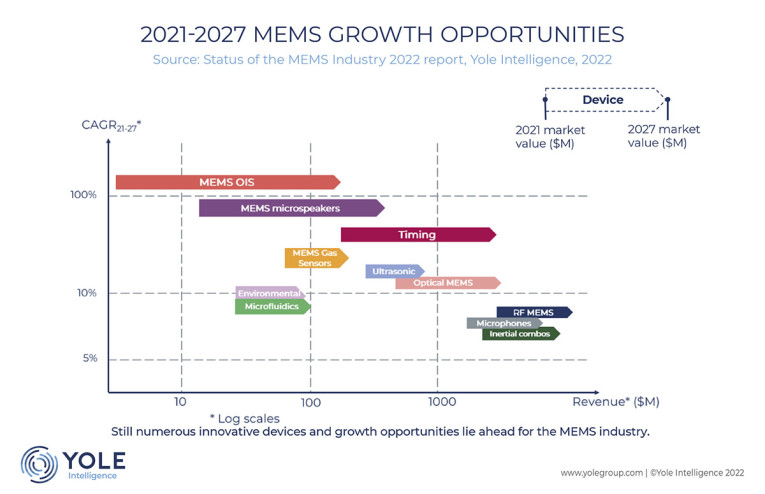

- A strong demand for MEMS, with some MEMS foundries’ schedules already filled to end-2023;

- Decreasing margins because of higher operating costs due to the current microeconomic and macroeconomic situation leading to an increase in ASP across some MEMS devices;

- And future inventory over-stocking by integrators stockpiling chips (among them MEMS), potentially leading to a downturn in MEMS players’ activities in 2023 and later.

"Thus, a message to the participants in the ever-evolving MEMS industry: please tread carefully ahead," Damianos warns.

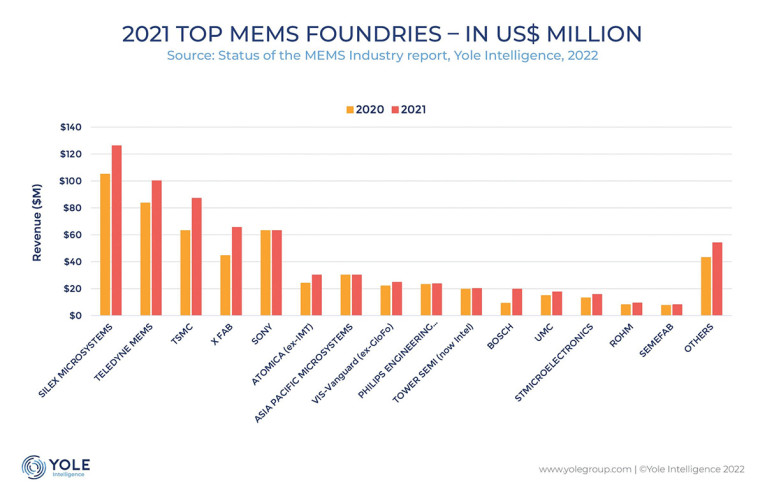

This new edition of the Status of the MEMS Industry report details the latest updates on MEMS volumes, ASPs, and revenues for calendar 2021. It provides an overview of MEMS’ best future growth opportunities and key market drivers for the next 5 years. It also offers a detailed view of the ecosystem development in terms of both products and funding and the main stakeholders involved. A detailed analysis of MEMS market shares is included, along with an analysis of the foundry business, giving a comprehensive view of the MEMS ecosystem.

Yole Group will be a main presenter at the MEMS & Imaging Sensors Summit powered by SEMI, taking place 6-7 September, 2022 in Grenoble, France.

More info here.

Yole Group is an international company specializing in the analysis of markets, technological developments, and supply chains, as well as the strategy of key players in the semiconductor, photonic and electronic sectors.

www.yolegroup.com