The corporate meeting room has been a major growth vertical market for audio visual technology. With significant developments, end users are now able to choose from a wider range of technologies and feature sets going into meeting rooms. The market is also demanding and adopting a broader spectrum of feature sets and technologies than ever before.

Bringing perspective to this rapidly evolving landscape is the 3rd iteration of Futuresource’s Meeting Room Technology End User report. In 2014, Futuresource conducted an in-depth study into the trends, usage drivers, product positioning and market outlook for display products and associated technologies, interviewing 500 IT and AV managers of large, medium and small corporates in the USA, France, Germany and the UK. The 2016 report provided an updated view and point of comparison for AV usage developments within the corporate sector and expanded to include the view-points of end users.

The report highlights trends in the display segment, divided into Projectors, Flat Panels, and Interactive Displays, Control Systems, Room Booking Systems, Environment Controls (HVAC/Lighting), AV Signal Distribution (Matrix & AV Over IP), Collaboration Solutions such as Wireless Presentation Devices, Video Conferencing, Interactive Displays, PTZ Cameras, and Audio Technologies in the areas of Telephony, Microphones, and Speakers.

This report builds on the success of previous reports using a distinct methodology. This mixture of AV decision makers and end-users provides invaluable insight into the make-up and use of technology in meeting rooms. In addition, this report looks to expand understanding of meeting room technologies, placing increased focus on product categories such as video conferencing, wireless presentation solutions, speakers, microphones and telephony, while ensuring that the emphasis on displays is unhindered. In addition, this report provides perspective on the current and future adoption of an expanded list of meeting room technologies.

Finally, this report supplements findings from end user research, with expert interviews with manufacturers of meeting room solutions and insights from Futuresource market tracking services to provide a holistic perspective of technology adoption in the corporate meeting room. This allows a perspective on the Total Addressable Market (TAM) and segment by room type/company size, including formal "huddle" meeting spaces, existing technology market penetration (for display, control, collaboration and audio technologies), product lifecycle and drivers.

The report also looks at the competitive situation between display and collaboration technologies and key issues driving corporate applications, including choice by room type, 2018 budget expectations, channels used for purchase and key influencers on the purchase process, as well as current adoption and future expectations for investment in meeting room technologies.

“Over the past 5 years, Futuresource has been tracking the corporate meeting room technology space and the landscape has evolved rapidly, with the market demanding a broader spectrum of feature sets and technologies than ever before. This change in adoption and use case has brought an increasing number of solution providers from different parts of the AV/IT market into the meeting room,” comments Anthony Brennan, Research Analyst at Futuresource Consulting.

With nearly 11 million meeting rooms in Western Europe and North America, businesses are seeking to create engaging, flexible, physical and digital work spaces that promote interaction, collaboration, productivity and innovation across departments. Functions and technologies like IT systems, interactive displays, video conferencing, wireless presentation solutions, professional audio and room control devices continue to grow in significance, as this latest study certainly reaffirms.

"It is not just about firms blindly investing in the ‘latest and greatest’ when planning meeting room technology, it is much more than that. It is about the blending together of both physical and digital to foster synthesis and innovation in the workspace. This is critical for employee success which is in turn key to business accomplishment, and firms realize this,” adds Brennan.

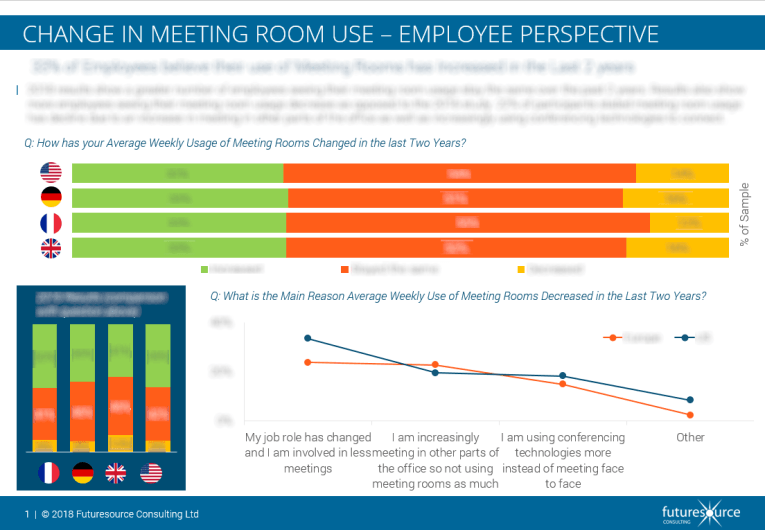

Over 2,500 end-users and decision makers from the USA, UK, France and Germany were interviewed to gain perspectives on the demographics of meeting rooms, use of meeting room technologies, budgeting and purchasing of technologies and end-user behavior.

Trends in Meeting room technologies

Amongst widespread technological innovations, devices used in meeting rooms have evolved significantly in recent years, with spending on products diversifying as a result. Meeting room budgets are increasingly being distributed to cover a broader range of technologies, with respondents seeing an increase in spending on products beyond displays, for example audio, collaboration devices and control products. With a growing number of solutions on the market and increasing appetite amongst end-users for a range of technologies, vendors from a wide range of disciplines and backgrounds are increasingly targeting opportunities in the corporate sector.

Despite the vast opportunities available, challenges remain. This is particularly evident in the growing trend amongst major providers to incorporate a wide range of functionalities into a single device. A good example of this has been the development of video conferencing soundbars from companies like Yamaha and Harman. With nearly 50% of spending in small meeting rooms attributed to devices outside display technologies, it is easy to understand the unique selling point of devices that seek to cover more of an end-users meeting room needs.

The results highlight that there is a very good reason for the widespread attention paid to ‘huddle spaces’ and small meeting rooms. While defining a ‘huddle space’ remains challenging, small meeting rooms sitting up to 6 people accounts for 49% of meeting rooms in Western Europe and North America. Beyond these dedicated spaces, respondents state that 20% of meetings are being held in non-traditional areas such as in kitchens, breakout spaces, receptions and foyers, a clear opportunity for vendors to tap into.

These spaces drive both informal and productive interaction, allowing for faster and more flexible meeting scenarios. Given the widespread nature of these meetings it is important for vendors to reflect on the impact that this may have on the market, particularly considering that 43% of companies surveyed stated that they are investing in technology for meetings held outside of meeting rooms. “Furthermore, a good example of the impact of these spaces could be seen in the US. While much of the investment made is for Wi-Fi access, the USA saw a much higher propensity to invest in conferencing technologies for huddle areas, presenting a significant opportunity for vendors,” adds Brennan.

The report also found that a growing number of employees are joining meetings remotely, with 11% of employees working from home three or more days a week and 32% of respondents reporting an increase in the average amount of time spent meeting remotely via conferencing technology on a weekly basis.

This trend has impacted not only the demand for conferencing technology but has also developed the need to collaborate and share content across operating systems and platforms from a distance. This has driven new product demands, for example building in wireless content sharing to web conferencing platforms is now increasingly common and again highlights the integration of once standalone technologies.

The Futuresource report also goes into much further detail, covering additional trends and preferences relating to such things as remote working; video conferencing; the importance of the AV Channel; flat panel adoption; and digital signage.

More information available here.

www.futuresource-consulting.com